Why Lower Drawdowns Matter More Than Higher Returns?

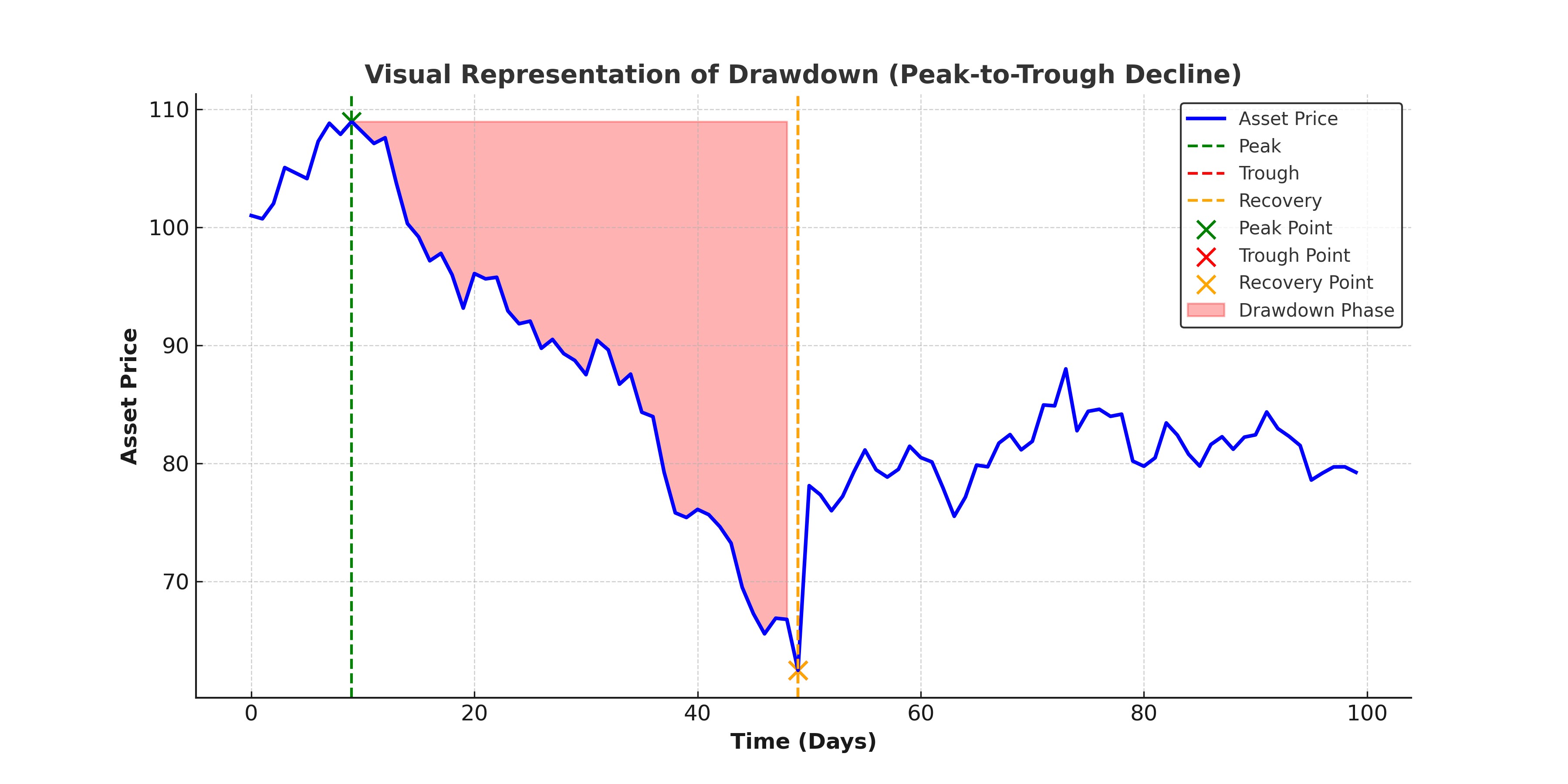

Drawdown refers to the decline in the value of an investment, portfolio, or asset from its highest point (peak) to its lowest point (trough) over a specific period. It is commonly used in risk management to assess potential losses and the volatility of an investment.

BOSSINVESTOR

Tue Mar 18 2025

Understanding Drawdowns

Drawdown refers to the decline in the value of an investment, portfolio, or asset from its highest point (peak) to its lowest point (trough) over a specific period. It is commonly used in risk management to assess potential losses and the volatility of an investment.

Key Characteristics:

- Measured from a peak to the subsequent trough before a recovery.

- Expressed as a percentage to indicate the extent of the decline.

- Helps in evaluating risk exposure in trading and investing.

Successful investing revolves around outperforming the market during favorable conditions while minimizing losses during downturns. This consistency is the foundation of long-term success. While drawdowns are inevitable, controlling them is essential for wealth preservation.

The Impact of High Drawdowns

A high drawdown can have serious consequences, both psychologically and financially. It affects investors' decision-making, portfolio recovery time, and overall long-term returns. Let’s break this down into key areas:

Psychological Impact of High Drawdowns

When investors experience a major drawdown, emotions take over, often leading to:

- Fear & Panic Selling – Investors may sell at the lowest point, locking in losses.

- Emotional Decision-Making – Instead of following a strategy, investors may react impulsively.

- Loss Aversion Bias – People feel the pain of losses more than the joy of gains, leading to irrational behavior.

Example: During market crashes, many investors panic sell, missing out on the recovery phase.

Impact on Long-Term Returns

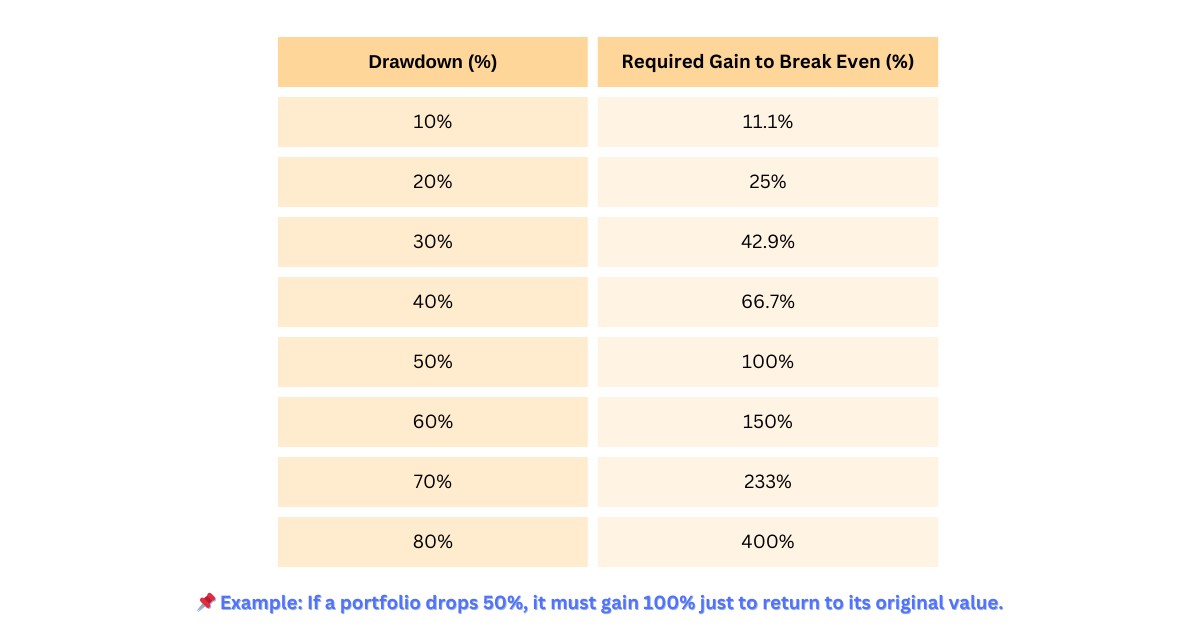

One of the biggest dangers of a high drawdown is the difficulty of recovering from losses. The larger the drawdown, the harder it is to break even.

Key Concept: The Loss-Recovery Rule

A drawdown requires a disproportionately higher gain to recover:

Opportunity Cost

A portfolio in drawdown often takes years to recover. This leads to:

- Missing New Investment Opportunities – Stuck in recovery mode instead of capitalizing on new market trends.

- Reduced Compounding Effects – Growth slows as time is spent recovering lost value.

- Lower Future Returns – The portfolio might never reach its full potential.

Example: If an investor’s money is locked in a drawdown, they miss out on a strong bull market.

Why Lower Drawdown is More Important

Managing drawdowns effectively is key to long-term financial success. A lower drawdown means better capital preservation, stronger compounding, and reduced risk of ruin. Let’s break it down:

Preservation of Capital (Protecting Your Nest Egg)

The #1 rule in investing is: Don’t lose money! The more you lose, the harder it is to recover.

- Lower drawdowns mean fewer drastic losses, allowing investors to protect their capital.

- Retirees and conservative investors rely on capital preservation to sustain their withdrawals.

- Example: If two investors start with $100,000:

Investor A loses 10% → Needs 11.1% to recover.

Investor B loses 50% → Needs 100% to recover.

Lesson: The deeper the drawdown, the harder and longer the recovery.

Compounding Effect: Why Stability Wins

Compounding works best when losses are minimized. A stable portfolio with consistent positive returns outperforms a volatile one over time.

- Compounding favors lower volatility. A portfolio that fluctuates wildly is less efficient.

- Example: A portfolio that grows 8% per year with low drawdowns will outperform one that has wild swings from +20% to -15%.

Key takeaway: The smoother the growth curve, the more wealth accumulates over time.

Reduced Risk of Ruin (Avoiding Catastrophic Losses)

A high drawdown can wipe out an investor's ability to stay in the market. This is especially risky for:

- Retirees – A large loss early in retirement can mean running out of money.

- Traders & Hedge Funds – A single deep drawdown can force liquidation (margin calls).

- Long-term Investors – Large losses can emotionally push them to exit the market at the wrong time.

Example: Many investors who sold during the 2008 crash missed the massive recovery that followed.

Achieving Financial Goals with Greater Certainty

A portfolio with low drawdowns and stable returns allows investors to:

- Plan better – Retire on schedule without financial surprises.

- Stay invested – Avoid panic selling during market crashes.

- Reach long-term goals faster – Higher certainty in wealth accumulation.

Example: An investor saving for a house or retirement benefits from predictable growth rather than extreme fluctuations.

Strategies for Minimizing Drawdown

Minimizing drawdowns is essential for preserving capital, reducing volatility, and maximizing long-term gains. Below are key strategies to help manage and reduce drawdown risk effectively:

Diversification (Spreading Risk Across Assets & Classes)

"Don’t put all your eggs in one basket." Diversification helps smooth returns by reducing exposure to any single asset’s poor performance.

- Asset Allocation: Balance stocks, bonds, real estate, and cash.

- Sector Diversification: Spread investments across industries (Tech, Healthcare, Consumer Goods, etc.).

Example: During the 2008 financial crisis, government bonds and gold outperformed stocks, helping diversified investors reduce losses.

Risk Management (Stop-Loss Orders & Position Sizing)

Proper risk management ensures that no single investment can cause a devastating loss.

- Stop-Loss Orders: Automatically sell a stock if it drops below a set price, limiting potential losses.

- Position Sizing: Never risk too much on a single trade—typically 1-2% of portfolio per trade.

- Portfolio Rebalancing: Periodically adjust allocations to avoid overexposure to risky assets.

Example: A trader using a stop-loss order at 10% avoids a 50% drawdown if a stock crashes.

Value Investing (Buying Undervalued Assets with a Margin of Safety)

Investing in undervalued, high-quality companies reduces downside risk.

- Margin of Safety: Buy stocks trading below intrinsic value.

- Low Debt & Strong Cash Flows: Choose companies that can withstand downturns.

Example: Warren Buffett’s value investing strategy helped him avoid excessive drawdowns in high-risk stocks.

Tactical Asset Allocation (Adjusting Investments Based on Market Conditions)

Unlike static portfolios, tactical asset allocation (TAA) adjusts investments based on market trends.

- Increase cash holdings before expected downturns.

- Shift into defensive sectors (Utilities, Consumer Staples) during volatile times.

- Rotate into growth stocks during bull markets.

Example: During economic uncertainty, hedge funds rotate out of growth stocks and into bonds to reduce drawdowns.

Sticking to a Well-Defined Investment Strategy

Having a clear investment strategy and sticking to it prevents emotional decision-making.

- Define your risk tolerance and investment horizon.

- Create a written investment plan to follow in all market conditions.

- Avoid chasing hot stocks or panic-selling during downturns.

Example: Long-term investors who stayed in the market after the 2008 crash saw their portfolios recover and grow significantly.

The Role of Investor Psychology

Investor psychology plays a crucial role in minimizing drawdowns and achieving long-term success. Emotional reactions like fear and greed can lead to costly mistakes, while a disciplined, long-term approach helps investors navigate market volatility.

Importance of Emotional Control (Avoiding Fear & Greed)

Emotions drive many investment decisions, often leading to buying high and selling low—the exact opposite of a good strategy.

- Fear: Investors panic during downturns and sell at the worst time.

- Greed: Investors chase hot stocks or bubbles, often buying at the peak.

- Overconfidence: Thinking "this time is different" can lead to excessive risk-taking.

Example: During the 2008 financial crisis, many investors panic-sold their portfolios at the bottom, missing the historic recovery.

Solution: Stick to a predefined investment plan and avoid emotional decision-making.

Long-Term Perspective (Focusing on Goals, Not Short-Term Fluctuations)

Short-term market movements are unpredictable, but long-term trends favor disciplined investors.

- Market volatility is normal – Ups and downs are part of investing.

- Stay focused on long-term goals – Retirement, wealth building, financial security.

- Avoid excessive trading – Frequent buying and selling increases costs and emotional stress.

Example: The Nifty 500 has returned ~12% annually over the long term, despite multiple crashes. Long-term investors who stayed invested saw their portfolios recover and grow.

Solution: Adopt a buy-and-hold strategy and ignore short-term noise.

Understanding Market Cycles (Recognizing That Downturns Are Normal)

Markets move in cycles—bull markets (rising prices) and bear markets (falling prices). Recognizing this helps investors stay calm during downturns.

- Boom & Bust: Every market cycle has ups and downs.

- Bear Markets Are Temporary: Historically, they last ~1-2 years, while bull markets last longer.

- Recessions & Corrections Are Opportunities: Smart investors buy when others panic.

Example: The COVID-19 crash in March 2020 saw markets drop 35% in weeks—but the recovery was swift, reaching new highs in 2021.

Solution: Accept market cycles and use downturns as buying opportunities instead of panic selling.

Seeking Professional Advice (Guidance from Financial Advisors)

A financial advisor can help investors stay objective and avoid emotional mistakes.

- Behavioral Coaching: Helps prevent panic selling and impulsive decisions.

- Portfolio Management: Advisors create a diversified, risk-adjusted portfolio.

- Personalized Financial Planning: Tailor strategies to long-term goals and risk tolerance.

Example: Studies show that investors who work with advisors tend to have better long-term returns due to fewer emotional mistakes.

Solution: If unsure, consult a financial professional to stay on track.

Final Thought

Prioritizing lower drawdowns over chasing high returns is the key to long-term investing success. By managing risk effectively, you ensure smoother portfolio growth, reduced stress, and the ability to stay invested through market cycles. Remember, consistency beats volatility.